Are you daydreaming about the day you can call a place your own? The allure of homeownership often leads many to contemplate tapping into their 401(k) savings to secure a down payment. While the numbers might seem promising, taking a closer look at the implications is crucial before making a decision. Before you decide to dip into your retirement savings for a home, be sure to consider all possible alternatives and talk with a financial expert. Here’s why.

The Temptation of Numbers

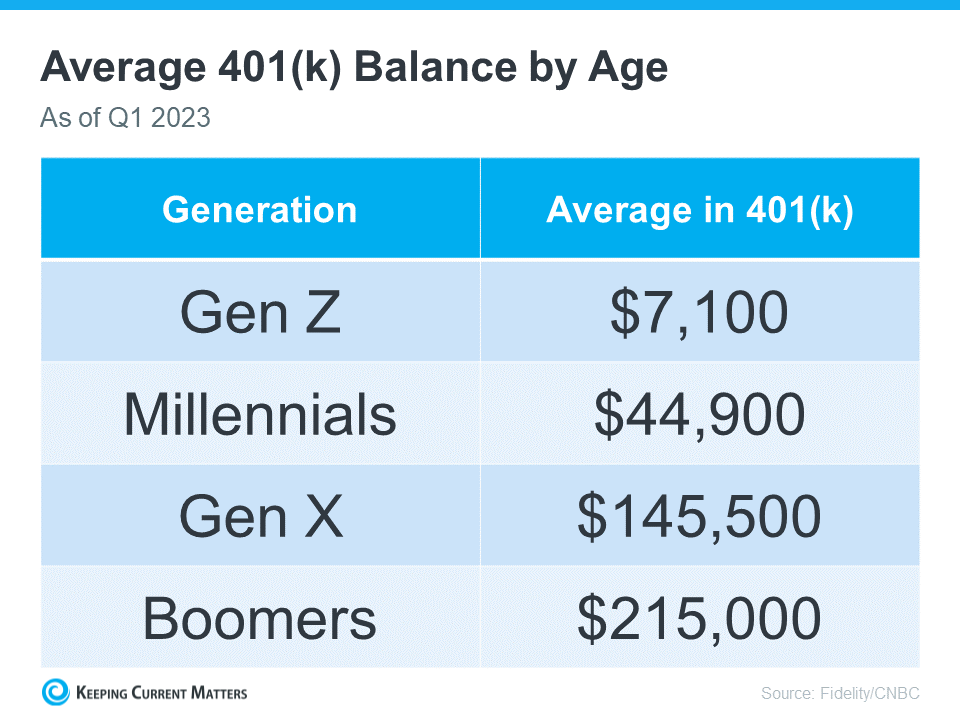

Many Americans have diligently saved for retirement, accumulating a significant nest egg in their 401(k) accounts. It’s a tempting prospect when you witness your dream home materializing on the horizon. However, it’s vital to tread carefully, as dipping into your retirement savings for a home could result in penalties and potentially impact your financial future. According to Experian:

“It’s possible to use funds from your 401(k) to buy a house, but whether you should depends on several factors, including taxes and penalties, how much you’ve already saved, and your unique financial circumstances.”

Exploring Alternatives

While using your 401(k) is one way to finance a home, it’s by no means the only option. Before making a decision, consider alternative methods, such as:

- FHA Loan: FHA loans allow qualified buyers to put down as little as 3.5% of the home’s price, depending on their credit scores.

- Down Payment Assistance Programs: Numerous national and local programs exist to aid first-time and repeat homebuyers in coming up with the necessary down payment.

Above All Else, Have a Plan

Regardless of the path you choose to purchase a home, consulting a financial expert is crucial before taking any action. Developing a concrete plan with a team of experts before embarking on your homeownership journey is the key to success. Kelly Palmer, Founder of The Wealthy Parent, emphasizes the importance of having a tangible plan:

“I have seen parents pausing contributions to their retirement plans in favor of affording a larger home often with the hope they can refinance in the future… As long as there is a tangible plan in place to get back to saving for their retirement goals, I encourage families to consider all their options.”

Bottom Line

If the idea of using your 401(k) for a home down payment is still on your mind, take the time to explore all your options and consult with a financial professional before making any decisions. Your dream home is within reach, but the journey should be a well-thought-out and strategic one.

*Info provided by Keeping Current Matters

Leave a comment